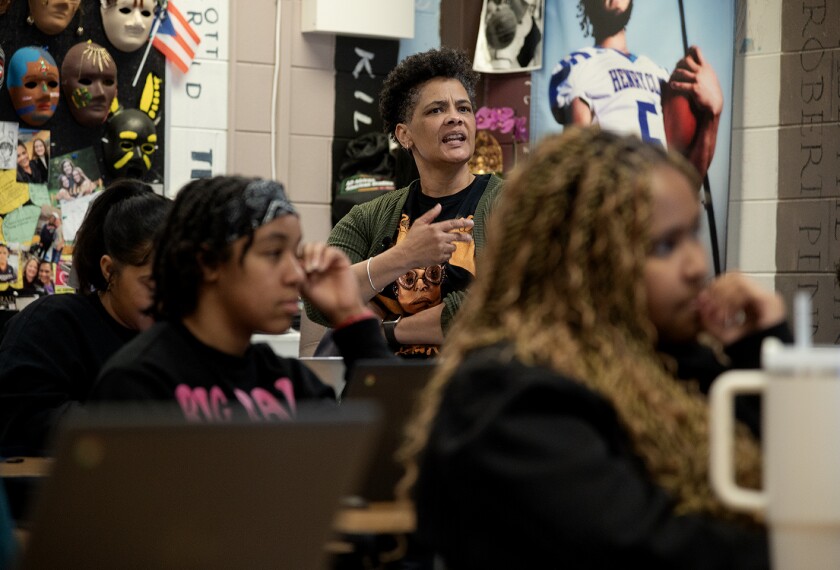

At Thomas S. Wootton High School, the raucous voices of students fill the air, peppered with the buttery smell of hot popcorn, pizza, and steamed hot dogs. But juniors Jeremy Baine and Michelle Song aren’t eating lunch. Instead, they’re working as tellers at the school’s credit union branch.

|

| Left, high school juniors Jeremy Baine and Michelle Song work as bank tellers in a credit card union inside Thomas S. Wootton High School in Rockville, Md. —Photograph by Allison Shelley/Education Week |

Sixteen-year-old Ron Golan lopes in and sits below the red, white, and blue banner proclaiming “Patriots’ In-School Credit Union.” He plunks down a wad of cash before Ms. Song, who carefully counts out $400, then gives him a deposit slip.

Business teacher Lloyd Ryan stands nearby, monitoring the tellers. About 100 students have opened accounts at the branch since it opened in November.

“This is a learning tool for students,” Mr. Ryan said. “We want to teach kids [financial] responsibility.”

The credit branch at this 2,250-student school in suburban Washington is just one sign that financial literacy is starting to gain traction in schools nationwide. This national push to teach personal-finance skills is the result of a growing awareness that most students don’t know the basics about money management, leaving them vulnerable in an increasingly sophisticated world that offers a dizzying array of financial choices.

“This has become a front-page issue,” said Robert F. Duvall, the president and chief executive officer of the New York City-based National Council on Economic Education. “There is growing recognition that we’ve got a problem.”

States Take Action

At least sixteen states have passed legislation over the past year requiring some sort of financial education in K-12 schools, while nine states have similar legislation pending, according to the Jump$tart Coalition, a Washington-based nonprofit group that’s working to improve the personal financial literacy of young adults.

On the national level, Congress recently established a high-level commission—which includes U.S. Treasury Secretary John W. Snow and the heads of the federal banking agencies—to coordinate federal agencies’ efforts to improve financial literacy for both students and adults.

Congress also passed the Excellence in Economic Education Act, a $1.5 million program to increase students and teachers’ understanding of economic education and to expand its support nationwide. It is an addendum to the No Child Left Behind Act.

Democratic Sen. Daniel K. Akaka, of Hawaii, a co-sponsor of the economic education act, emphasized the need for stronger measures in a subcommittee financial-management hearing in Washington in March.

“Americans of all ages and backgrounds face increasingly complex financial decisions,” he said. “Many find these decisions confusing and frustrating because they lack the tools necessary that would enable them to make wise, personal choices.”

Financial companies and credit unions have also pitched in to educate students. New York City-based Merrill Lynch & Co. Inc. recently devised a 15-lesson curriculum and video series on personal finance, aimed especially at urban students in elementary, middle, and high school. And Citigroup Inc., also based in New York City, recently announced that it will spend $200 million to underwrite consumer education programs, many targeting students, around the world.

The Montgomery County Teachers Federal Credit Union, which oversees Wootton High’s branch, has six such mini-branches in schools in the Maryland jurisdiction. And the State Department Federal Credit Union, based in Alexandria, Va., has also trained nearby elementary students and teachers in that state to operate their own in-school branch.

The economic slowdown of recent years makes it all the more important for students to learn how the financial world works, said William Cook, the vice president for operations and development at the State Department Federal Credit Union.

“It’s important to educate people in their youth,” he said.

‘Very Complex Subject’

The increased attention paid to financial literacy couldn’t come at a better time, say many experts. Schools, they point out, historically have not taught personal-finance skills, and it shows.

Bankruptcy rates have doubled over the past decade: More than 1.6 million people filed for personal bankruptcy between September 2002 and September 2003, a 7.5 percent increase from the previous year.

The average college senior has $3,262 in credit card debt, according to an April 2002 analysis by the student-loan corporation Nellie Mae, based in Braintree, Mass. In addition, 21 percent of all college students carry credit card balances between $3,000 and $7,000, a 61 percent increase from 2000.

Not surprisingly, high school seniors have scored 52.3 percent, on average, or lower since 2000 on a national test of personal-finance knowledge produced by the Jump$tart Coalition.

That’s a failing grade, said Lewis Mandell, the researcher for the test and a professor of finance and managerial economics at the University of Buffalo school of management in New York.

He was heartened to see that this year’s results are slightly better than last year’s 50.2 percent. Still, he said, young people have a long way to go.

“Finance is a very complex subject,” Mr. Mandell said. “It’s not unlike mathematics or French. … It builds on things you already know, and it takes discipline and hard work to master it.”

Only 35.3 percent of the more than 4,000 high school seniors surveyed noted correctly that a state bond is not federally protected against loss. And only 46 percent correctly answered that older people living on a fixed-retirement income—not young working couples with children or older working couples—would be most affected during a high inflationary period of several years.

Experts say one reason students have such an abysmal working knowledge of personal finance is that they’re not learning about it at home, said Mr. Mandell. Unfortunately, he said, that’s because many adults know little more than their children.

“A lot of adults screw up their own finances,” Mr. Mandell said. “How many parents know how to teach this stuff to their children?”

Knowing how to manage your money effectively, as well as knowing how the free-market economic system works, is more important now because the national economy is increasingly affected by the global economy, experts point out. And the number of financial vehicles and tools the average American must track and understand—such as individual retirement accounts and credit cards—has soared.

“When we bought our first house in the early 1970s, there was only one [type of] mortgage,” Mr. Mandell said. “It wasn’t ideal, but you couldn’t make too many mistakes. Nowadays, there are hundreds of different mortgages. It takes some real intelligence to know what is best for you.”

Laura Levine, the executive director of the Jump$tart Coalition, said not only are there more financial choices, but it can also be difficult to separate the wheat from the chaff because of increased advertising.

“The marketing of these financial products is more aggressive, so the need seems ever more urgent for young people to understand them,” she said.

Lack of Resources

The recent drive to promote financial literacy in schools is a good first step, but obstacles remain, experts say.

For instance, although more attention has been paid to promoting financial literacy at the state level, much of the legislation is unfunded, according to Mr. Mandell.

“And that,” he said, “doesn’t do any good for our kids whatsoever.”

Mr. Mandell also noted that many schools of education do not offer prospective teachers curriculum training on personal finance, nor do they show how to integrate it into subjects such as history and mathematics.

Many educators say the tendency in K-12 schools to focus almost exclusively on core academic subjects because of the increasing demands of the federal No Child Left Behind Act can push financial literacy to the sidelines. And some think that’s where it should be.

But others say it’s a subject that needs attention in the classroom.

“I’ve talked to principals and superintendents, and they say, ‘This is a problem. But I don’t have the people to teach it, and I don’t have the resources to pay for it,’ ” Mr. Mandell said.

Lunch was nearing its end at Wootton High when Mr. Golan pocketed the deposit slip that fellow student and credit union teller Ms. Song handed him. Before he headed out the door, he paused and said he regularly makes deposits into his checking account at school.

“It’s so much more convenient than going to a branch [off campus],” he said, then headed out the door, slipping into the lunchtime crowd.