Like overlapping board memberships, financial relationships do indicate related parties rather than mere social acquaintances. It is possible for individuals and organizations to act in concert de facto without overlapping boards or financial ties – or even direct conversations, especially in the pursuit of shared ideological and political objectives. Indeed, this is an essential ingredient of modern political campaigns – consider the “527s.” By the same token, one bank’s extension of home owner mortgages and business lines of credit to multiple parties implies it is possible to have close financial ties entirely at arms length.

The question is: what do we have here? Specifically, what are the financial relationships among the organizations discussed in my last posting? And for readers, what are the implications? Does the pattern of foundation grants suggest coordination, concerted action, a network, an alliance?

Foundations are the institutional financiers of the nonprofit world. Their grant decisions are no more random than any commercial investor’s; indeed, they are more narrowly grounded, Presumably, at least in the eyes of a foundation’s board of directors, grants are made in pursuit of the mission or purpose identified in the foundations articles, by-laws, mission statements to organizations with consistent missions and purposes. The competence and capacity of a prospective grantee’s management may well be less important than the social objective the nonprofit will pursue. Indeed aside from obvious profligacy, the grantee’s efficient stewardship of resources is rarely something a grantor knows with any certainty. Agreement with the grantees tperception of social need, consistency with the foundation’s philosophy, and some external measure of community support is generally the extent of philanthropic due diligence and accountability.

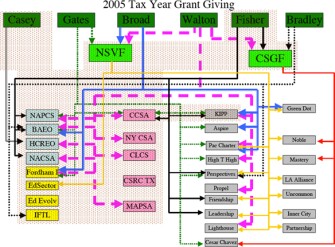

Below I’ve included a figure based on the IRS Form 990s filed by these organizations for Tax Year 2005. I have also expanded the list well beyond the few examples of Charter Management Organizations (CMOs) in the last post. This is the most recent data available for the whole group. It is complicated. Farther below a table based on those same forms provides the details.

Key:

• Shaded Area: The National Alliance of Public Charter Schools and the organizations its board members belong to.

• Foundations (Forest Green): Casey, Gates, Walton, Fisher, Bradley

• Financial Intermediaries (Lime Green): New Schools Venture Fund, Charter School Growth Fund

• Advocacy Groups (Blue): National Alliance for Public Charter Schools, Black Alliance for Educational Options, Hispanic CREO, National Association of Charter School Authorizers

• “Think Tanks” (Yellow): Fordham Institute, Education Sector, Education Evolving, Institute for the Transformation of Learning

• Charter School Organizations (Pink): California Charter School Association, New York Charter School Association, Charter School Resource Center of Texas, Michigan Association of Public Charter Schools

• CMOs (Grey): Knowledge is Power Program, Aspire Public Schools, Pacific Charter Development, High Tech High, Perspectives Charter Schools, Propel Charter Schools, Friendship Public Charter Schools, Leadership Public Schools, Lighthouse Academies, Cesar Chavez, Green Dot, Noble street, Mastery , LA Alliance for College Ready Schools, Uncommon Schools, Inner City Education Fund, Partnerships to Uplift Communities

2005 is a reasonable time to take a financial snapshot for several reasons. It is the year Education Sector was created and when the National Alliance for Public Charter Schools was formed out of the Charter School Leadership Council. It is also several years into the shift towards CMOs telegraphed in 2003 by New Schools Venture Fund founder Kim Smith, and so well into the shift of the philanthropies discussed here away from independent charters and towards these nonprofit school managers.

Notes on the Data

• Foundations are required to disclose each grant. Grantees are not required to disclose individual grants, but are required to identify private donations, government grants, and fees revenue. Most nonprofits, including “transparent” Education Sector, provide little further insight into sources and uses of funds. Almost all file incomplete forms and ask for extensions.

• Organizations have different fiscal years, some run from January to December; others track the school year and run September to August; some run July to June. Moreover, some nonprofits account on a cash basis, others on accrual.

• At least for nonprofits, many of the CMOs have complex financial arrangements, but don’t seem to “roll up” the accounting of these controlled entities like a conglomerate firm. I have set up “nonprofit supporting organizations” myself, so I would not imply that there’s anything wrong with this. There are reasons to isolate real estate transactions and schools – for one thing to assure that liability can be limited to a site or facility. I would only say that it makes it harder to construct a good picture of CMO finances without more time than I was prepared to invest.

Financial Dependence

Clearly, one of my objectives here is to examine the issue of financial dependence. I have tried to get at that with the column titled “Donations/Total Budget.” The analysis needs a bit if refinement, but I an confident that the order of magnitude and overall pattern are “directionally correct.” I will post refinements later

In the case of think tanks, grants are the only game in town. I’ve adopted the view that when an organization is getting more than 20% of funding from one source, it has crossed a threshold of dependency. Readers may differ.

Organizations that claim to represent others could draw financial support from that group. The greater percentage of expenditures they cover with grants – especially core expenses, the more dependent they are on the grantors. Again, I would argue that the 20 percent rule applies.

CMOs are a bit more complicated. Here there will be substantial fee revenues from government in the form of per pupil payments. However, the management infrastructure to support whatever number of schools the grantees proposed must be established before that goal is achieved, real estate may need to be developed, and whatever operating expenses the new schools have will be incurred in advance of payment. Grants fill these gaps. The question is how long this support will be required at what level. Initial growth targets, and even those in revised plans, tend to be missed in the school management business. It is hard to know at this point whether these grants are better thought of as permanent operating subsidies rather than temporary start up funds. In any case, to the extent that the CMO needs grants to cover its financial shortfalls, it is dependent on the grantors.

Observations:

• Pull Walton out of the equation and most organizations would shrink below critical mass. Many would disappear.

• Gates has made a significant investment in the group, but unlike Walton, 1) its important, but not fundamental and 2) this foundation gives to all kinds of organization in public education. Charter Schools were mainly an interest of Tom Vander Ark in the “small schools” context, and it seems likely that former NSVF Partner and EMO owner Jim Shelton was the key to this line of giving. (More on “people” and personal relationships in future postings.)

• The position of Broad is similar to Gates. Fisher is focused on a few important players. Pull one grantor out and there will be some damage to some organizations, but not the overall activity. Two or more exiting would be a serious problem. Casey and Bradley are small players, although Bradley’s grant to CSGF suggests it might get deeper into the space.

• New Schools Venture Fund is often viewed as an independent “philanthropy,” but it has become more of a financial intermediary – aggregating large grants and then re-granting those funds to other nonprofits. Charter School Growth Fund is the same kind of institution. What is important here is that both organizations are accountable to foundation for results and relevance. When the CMO idea goes the way of all trends in education philanthropy or if these intermediaries are seen to add more costs than value, NSVF and CSGF will be at risk.